In an earlier blog we covered the relatively slow move by European banks to modernize their systems over the last decade – a move now taking place at speed.

According to Mordor Intelligence, the European e-commerce gateway market will triple in value over the next five years, reaching $30 billion by 2030 – with growth like this, there’s everything to play for. The challenge for banks is that PSPs and fintechs have emerged as competitors fighting for the same revenues, because their brands are seen as being more agile and innovative. This leads to competitive pressure on banks and a struggle to retain market share as these more nimble players adapt more quickly to market demands and offer merchants attractive white-label solutions.

How banks can fight back

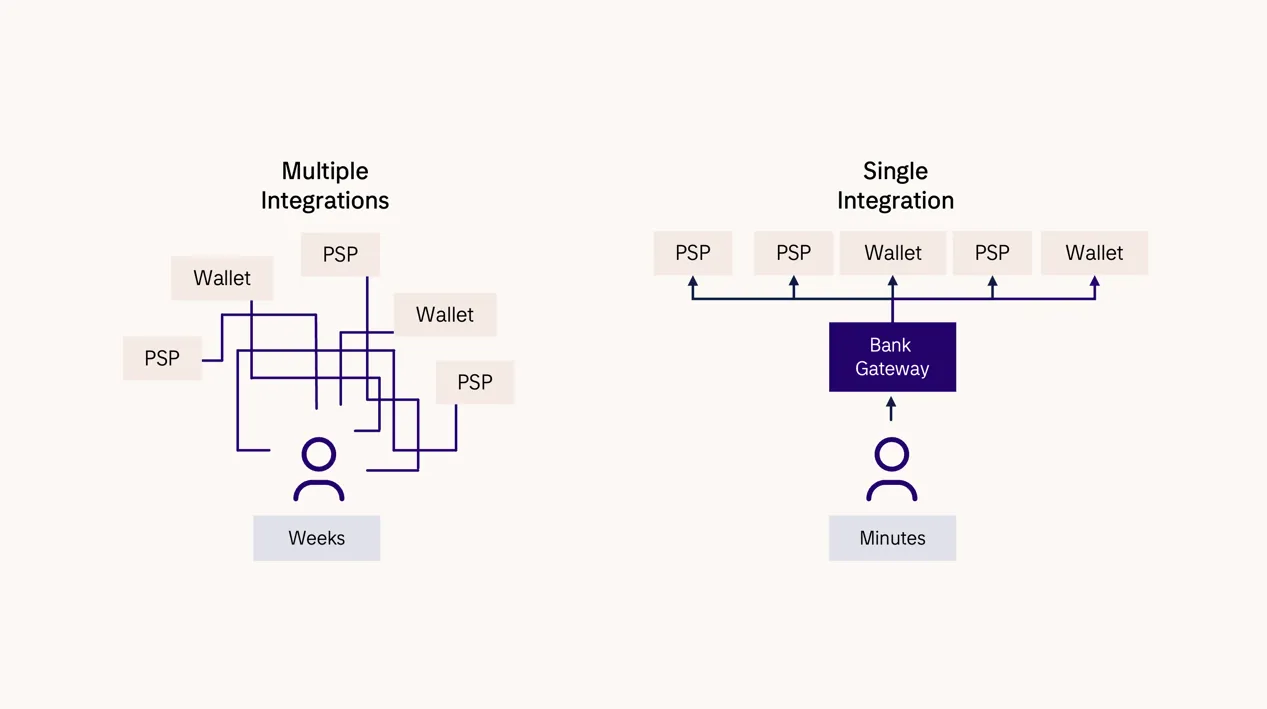

Even if their offerings seem attractive at first sight, PSPs and fintechs will typically offer a one-size-fits all model, which may not suit the specific needs of individual clients or markets. And while many PSPs or fintechs will claim to offer customization, this can be expensive and time-consuming, with merchants finding themselves stuck in a development queue that can last weeks or months. If merchants opt for a multivendor approach, things become even more daunting, as it adds the complexity of multiple integrations to the mix.

By owning merchant relationships with a bank whitelabel gateway, banks can create tailored features, from local payment methods through to creative features such as A2A transactions with a BNPL option, multi-function digital wallets, and more.

Alongside tailored features, banks can propose differentiated packaged solutions for specific verticals (think travel, hospitality or online gaming) which compare favorably with the “one-size-fits-all” approach of a fintech or a PSP. Own-label e-commerce gateways managed by banks with the support of a software partner typically involve a single integration – a feature which makes them attractive to merchants all by itself.

Add to that the fact that own-label gateways come with a scalable architecture, are cloud-ready and easy to integrate with ecosystem partners such as card schemes and third-party payment providers like PayPal, WERO, Blik, Bizum, Vipps, Swish, etcetera, and you have a compelling proposition for merchants.

Merchants also benefit from the reduced complexity of having their banking partner handle their payments, which makes reporting and reconciliation much easier.

Finally, bank-owned e-commerce gateways can be embedded as part of the merchant checkout process under the merchant’s brand, offering further value to the merchant while the bank manages processing and settlement and the bank’s software partner working to ensure a smooth, fast and secure payment experience.

At a time when fintechs and PSPs have seized the advantage, owning a proprietary e-commerce gateway enables banks to take the fight back to the market and regain competitive advantage in a market rich with opportunities over the next five years.