Plans, milestones, and… adoption?

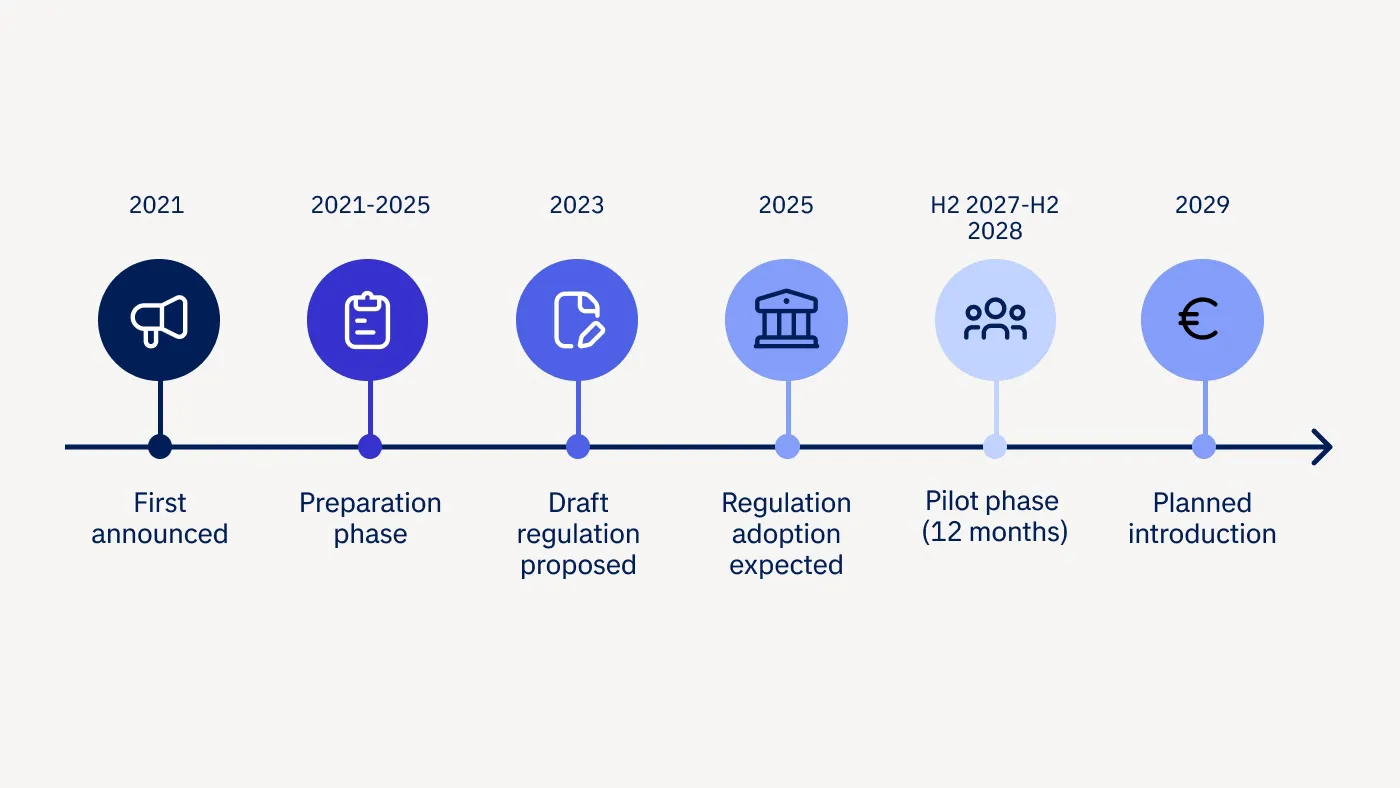

First announced in 2021, the digital Euro has been through a preparation phase that completed in 2025, including a draft rulebook, user research, and technical analysis. A draft regulation was proposed by the European Commission (EC) as early as 2023, which the European Parliament expects to adopt by the end of this year.

Assuming the regulation is adopted, the next step would be to pilot a digital Euro for 12 months from the second half of 2027. This pilot would involve selected banks and PSPs, and would help to troubleshoot any issues with a digital Euro from governance, systems, and functionality perspectives. Following this pilot, current plans are for a digital Euro to be introduced in 2029 – although the final decision rests with the European Council, and depends on the success of the planned 2027-2028 pilot.

What’s in it for banks – and what could go wrong

The case for a digital Euro includes the opportunity to reduce the cost of bank payments infrastructure in the longer term, and the capacity for payments innovation. As a fully programmable currency, banks could – for example – issue automatic refunds for cancelled services (e.g. concerts, travel tickets) and combine loyalty programs with payments, or embed payment with invoicing in areas such as utilities. Another argument positions the digital Euro as a pan-Euro-area platform for payments acceptance, providing an alternative to tech pays such as Apple Pay and non-bank options such as PayPal.

While the EC proposes to compensate banks for onboarding customers, systems maintenance, compliance, and processing, it wants investment from the banking sector of between €4–5.8 billion (€1–1.44 billion annually over four years). [1] Some banks are concerned that a digital Euro could lead to the loss of payment fees (such as card interchange) as consumers turn to real-time payments using the digital Euro.

Where banks stand – and what’s next

Industry organizations like the European Banking Federation believe banks should welcome the digital Euro. They are urging banks to prepare, arguing this will maintain their strong position as payments ecosystem providers in the future. Others are more skeptical: the EU is one of 146 countries and currency unions currently exploring the possibility of a Central Bank Digital Currency (CBDC), of which around half (77) have undertaken pilots or tests – but just three retail CBDCs have actually launched to date. [2]

![]()

The decision to introduce a CBDC can bring technical challenges and regulatory complexity. At present, many banks are weighing up the cost of preparing for a digital Euro against the perceived benefits. One unresolved question is the additional benefit of a digital Euro compared with standard instant payments – especially as instant payments begin to overlay new value-add services such as Request-to-Pay and credit products.

Banks that prepare proactively by upgrading their tech architectures and planning for new services based on the digital Euro will be best positioned to turn it into a net positive. During H2 2026 and early 2027, we expect the ECB to provide much more information on technical specs, liability and funding, and bank remuneration – all of which will help banks decide where to place their efforts.

[1] The European Central Bank, 27 March 2026: “Digital Euro – an opportunity for banks”: https://www.ecb.europa.eu/press/blog/date/2026/html/ecb.blog20260327~51b0640c39.en.html

[2] The Atlantic Council, June 2026: CBDC Tracker (live updates) : https://www.atlanticcouncil.org/cbdctracker/