Radical shifts in operating model required for a real-time era

European banks are moving beyond instant payments. In the near future, banks will have to navigate a wide ecosystem where all sorts of payments – bulk, high value, cross-border, and even direct debits – will be real-time. For several mid-to large-sized banks, the question is no longer whether the change is necessary, but whether they can move fast enough to avoid complicating a simple technology transformation into a long-haul, expensive operational burden.

With regulators mandating the adoption of instant payments and ISO20022 compliance, several banks were forced to take short cuts via workarounds on existing legacy systems just to achieve compliance on time. But this is an eighty-year-old with a chronic heart surviving on a pacemaker. Time is ticking and this is certainly not a permanent fix.

When workarounds stop working

Workarounds can be useful for a while as a quick fix to meet tight schedules but usually don't last long. Some of these systems are from the Victorian era – legacy systems built when cheques were still in use and payments were processed in days using files: not a suitable solution in a real-time world. As volumes continue to increase, these systems will either give up or the costs of operating them will erupt, as seen most recently in the three-fold cost increase for operating a mainframe ecosystem.

Mainframe operations have become disproportionately expensive as usage patterns change, and even the economics of just maintaining the platform can drift in the wrong direction. A legacy platform can start to look like a vintage car: valuable and familiar, but increasingly expensive to keep on the road.

At that point, hidden costs become harder to ignore. Teams age. Continuity risk rises. Resilience issues remain buried below the management layer.

The Great Hesitation, strategy, and the need for speed

The hesitation is understandable. Rebuilding or modernizing payments can feel like overhauling the engine of an aircraft while it is already in the air. The fear is not only technical; it is operational and emotional.

“The risk of doing something on time is easier to manage than the risk of not doing anything”

This hesitation is one of the reasons why payments modernization decisions are delayed. CIOs choose to keep the lights on in exchange for accepting a huge technical and operational debt.

One size doesn't fit all – why a tailored, agile approach suits best

Typically, big-bang migrations or modernizations go on forever without creating immediate value. What’s needed is a step-wise agile operating model scientifically tailored to a bank’s complexity, systems landscape, and ecosystem. In other words, an approach which makes the move more practical.

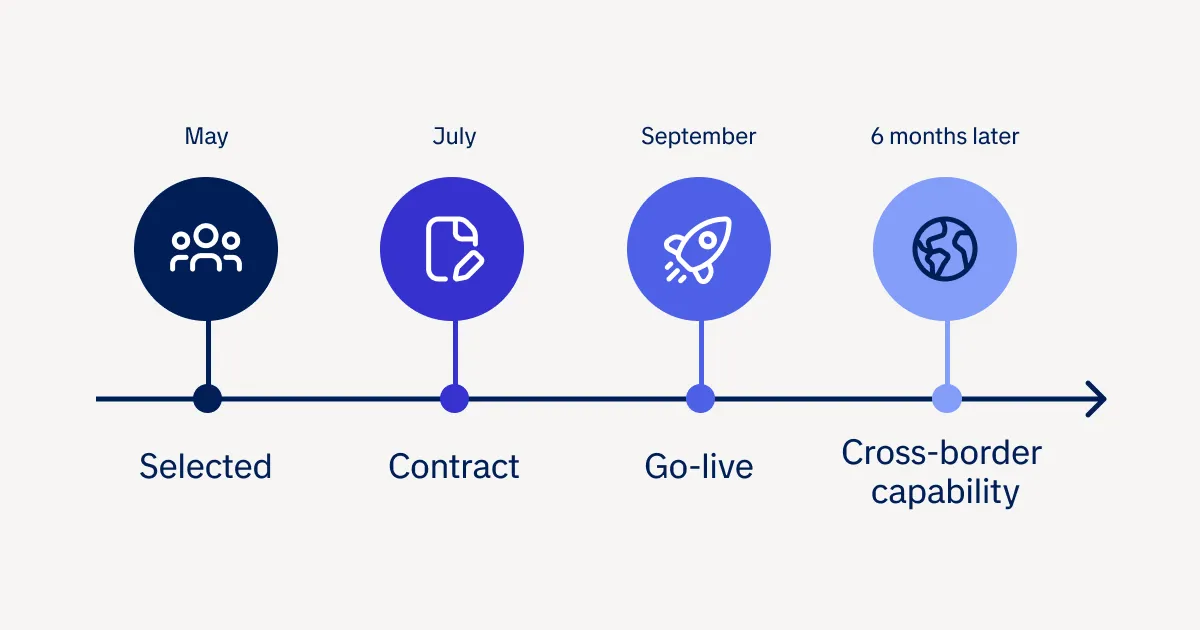

What speed looks like in practice

A client came to us with several legacy systems based in three different European countries. This was slowing down their ambition to become the most modern bank with a superior user experience.

Working with our client, we acted at speed, moving from preferred vendor selection to go-live in a just few months. We were selected in May, the contract was signed in July, and go-live happened in September. SEPA CT Instant Payments were delivered in roughly three months, and cross-border capability followed about six months later.

The bottom line

Change does not need to mean disruption for disruption’s sake. It should mean progress that is fast enough to matter, controlled enough to trust, and tailored enough to fit the bank’s business environment.

In that sense, the message is straightforward: the future of payments will not wait for long-haul transformation programs. Those banks that move in months, not years, will be the ones best placed to compete in the fast-emerging real-time era.