In this context, European banks must be ready to support multiple payment journeys simultaneously. For example, instant credit transfers via SCT-Inst demand for real-time payments, while direct debit remains essential for recurring and mandate-based collections. Meanwhile, Request to Pay adds a layer of customer interaction and control and high value, cross-border account-to-account flows remain crucial to global trade between companies, individuals and nations themselves.

In an instant world, orchestration is everything

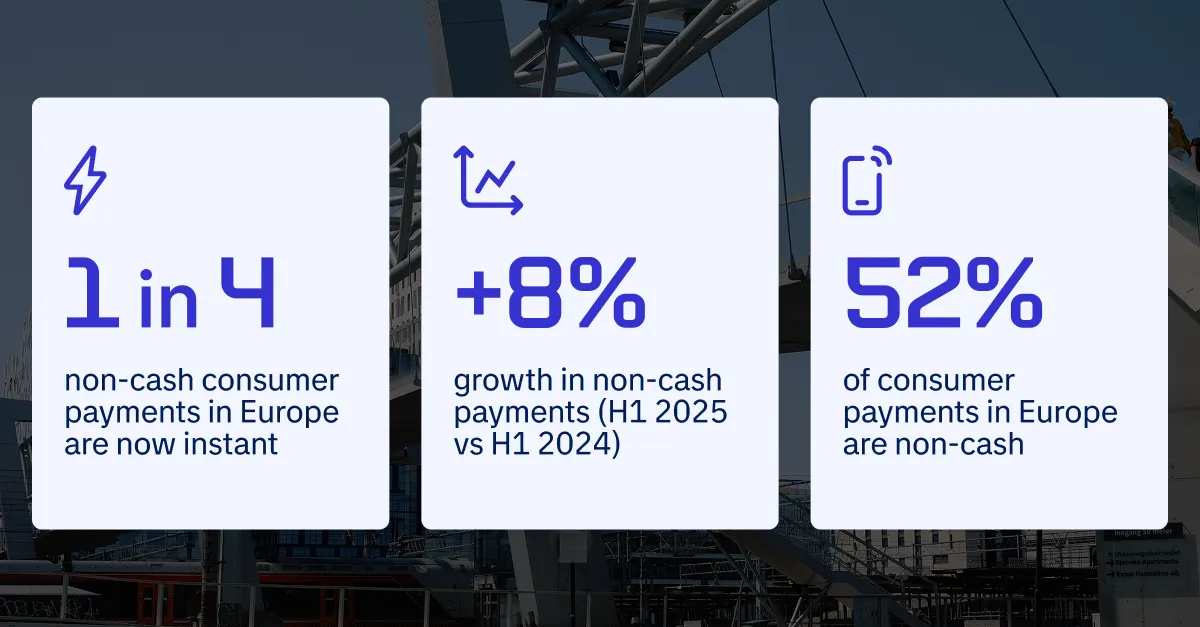

The opportunity for banks and payment companies is not to optimise each rail separately, but to orchestrate transactions coherently through a single, scalable transaction platform. As instant payments become standard and cash use declines, we can expect higher volumes of payment of all sizes to flow through transaction platforms – making the ability to operate at scale a strategic advantage. A couple of statistics illustrate this: in H1 2025, almost one in four non-cash consumer payments in Europe was instant, while non-cash payments grew by almost 8%, accounting for 52% of consumer payments alone.

Orchestration is not merely a concept or an Architecture - but represents a mindset shift and a new design approach that orchestrates several composable, built to evolve, atomic capabilities into a Robust and Resilient platform to Initiate, Validate, Process, Investigate and transmit payment of all sorts. This also helps banks to not just onboard a new scheme in no time, but also process thousands of transactions in fraction of a second.

Banks that comply with all current regulations may still be unprepared for the next wave of payment volume, complexity and customer expectation. The ability to support 10,000 transactions per second isn’t just good PR: rather, it’s evidence that the bank’s underlying infrastructure is prepared for the coming wave of higher instant-payment throughput, further cross-border expansion, a growing number of overlay services and relentless operational pressure. By equipping themselves to operate at scale, banks create a competitive advantage and prepare for the coming transition from card to A2A rails.

Digital currencies and assets matter – now

The same logic is shaping discussions around the digital Euro and digital assets. Debates about a digital Euro are not abstract policy discussions, nor are digital currencies a rarified payment form for restricted cases. Instead, these discussions should centre around resilience, standards, market structure, and reduced dependence on non-European technologies. The digital Euro is relevant right now, since it is a marker for what the market will expect from future payments infrastructure.

Looking ahead, European payments will be defined by whether we can execute multiple payment journeys on scalable infrastructure, which is resilient, capable, and built for Europe’s next strategic phase – fully sovereign payments in the digital era, delivered at industrial scale. To achieve this, banks don’t just need compliance with the latest regulations, or know-how: they need resilient, capable systems and a partner they can trust to deliver.