How digitalization is transforming corporate treasury

The aim of all treasuries is to increase operational efficiency and be recognised as an important part of the organisation to which they belong.

Being able to automate common daily treasury operations frees up treasury time, allowing staff to spend more time adding unique value to the organisation. Corporate size, location, and industry determine how treasury departments operate. Every treasury works differently, but most would agree that efficiency is key to success.

Becoming more efficient requires examining existing manual processes with a view to automate and improve them. Banks can and should partner with treasuries to help them meet these efficiency goals, not least by providing sophisticated automation and reporting tools. Exploring how digitalization can enhance treasury processes and seeking support from banking partners can help corporates on this journey.

As companies are pushed harder to do more with less, treasuries often take the lead in demonstrating the value of new technology and strengthening partnerships with their lead banks.

Why companies are centralizing treasury operations

Companies around the world face economic uncertainty and increasingly volatile markets. In response, many corporates are seeking to centralize core treasury activities to aggregate transaction flows and reduce risks across operating companies.

Moving from a decentralized treasury to a centralized in-house bank (IHB) model has become an aspiration for both large and smaller companies.

An IHB concentrates treasury activities, reducing external FX and cash transactions while minimizing the number of bank accounts and banking relationships. This not only optimizes treasury operations but also lowers costs.

A recent market study shows that 45% of companies globally have implemented an in-house bank. The main drivers include:

- Reduced costs

- Greater bank independence

- Lower operational risk by avoiding unnecessary cash movements

- Improved liquidity management

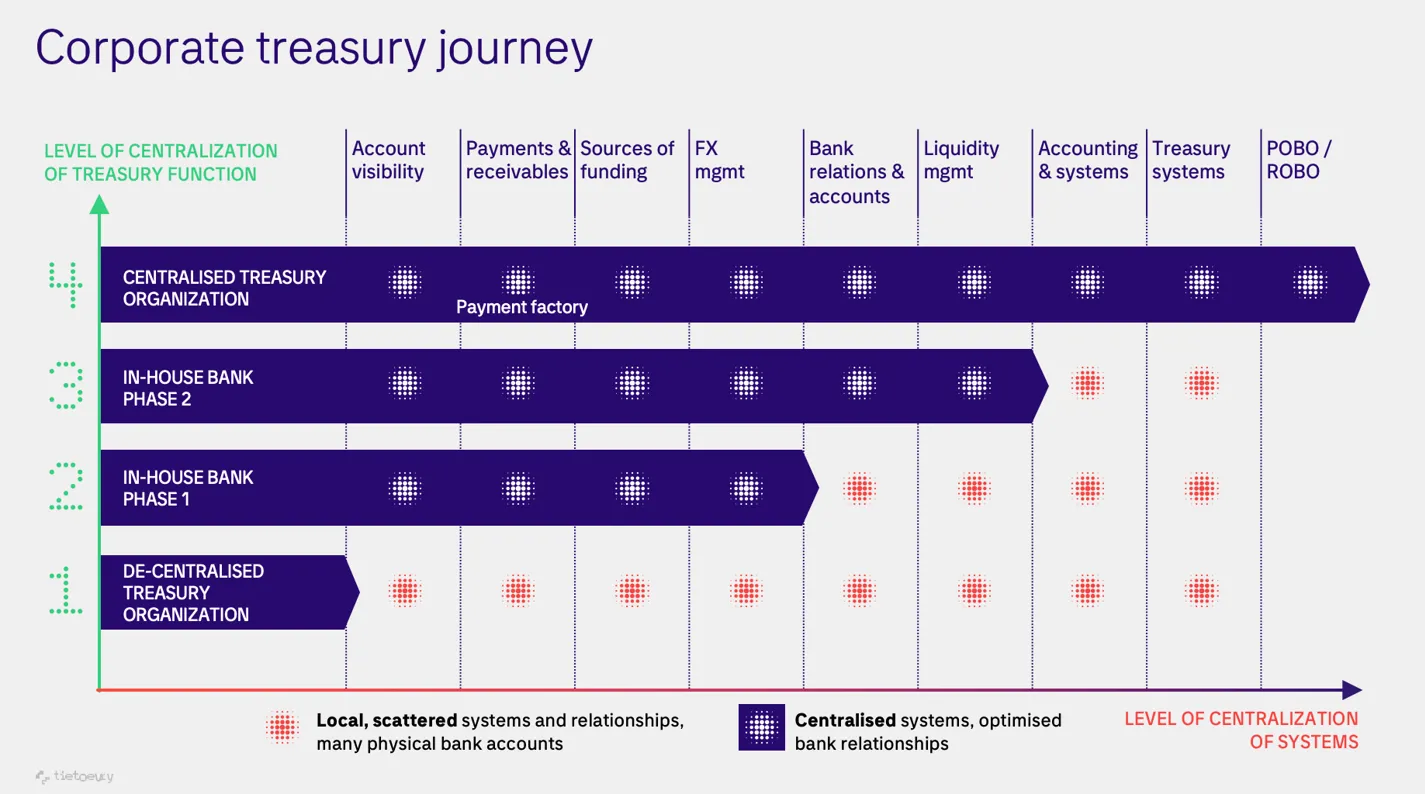

A phased approach to treasury centralization

Figure 1

Figure 1 illustrates how treasuries can move from a decentralized (step 1) to a fully centralized (step 4) operating model.

Not every transformation step is relevant for every company. Many organizations choose a phased approach, beginning with areas that deliver the greatest benefits, such as:

- Account visibility

- Centralized payments

- Funding

- Investments

Technology is central to this journey, making collaboration with treasury technology providers and banking partners increasingly important. Treasury management systems are often selected early in the project, with implementation synchronized alongside each transformation phase to ultimately support a single centralized treasury platform.

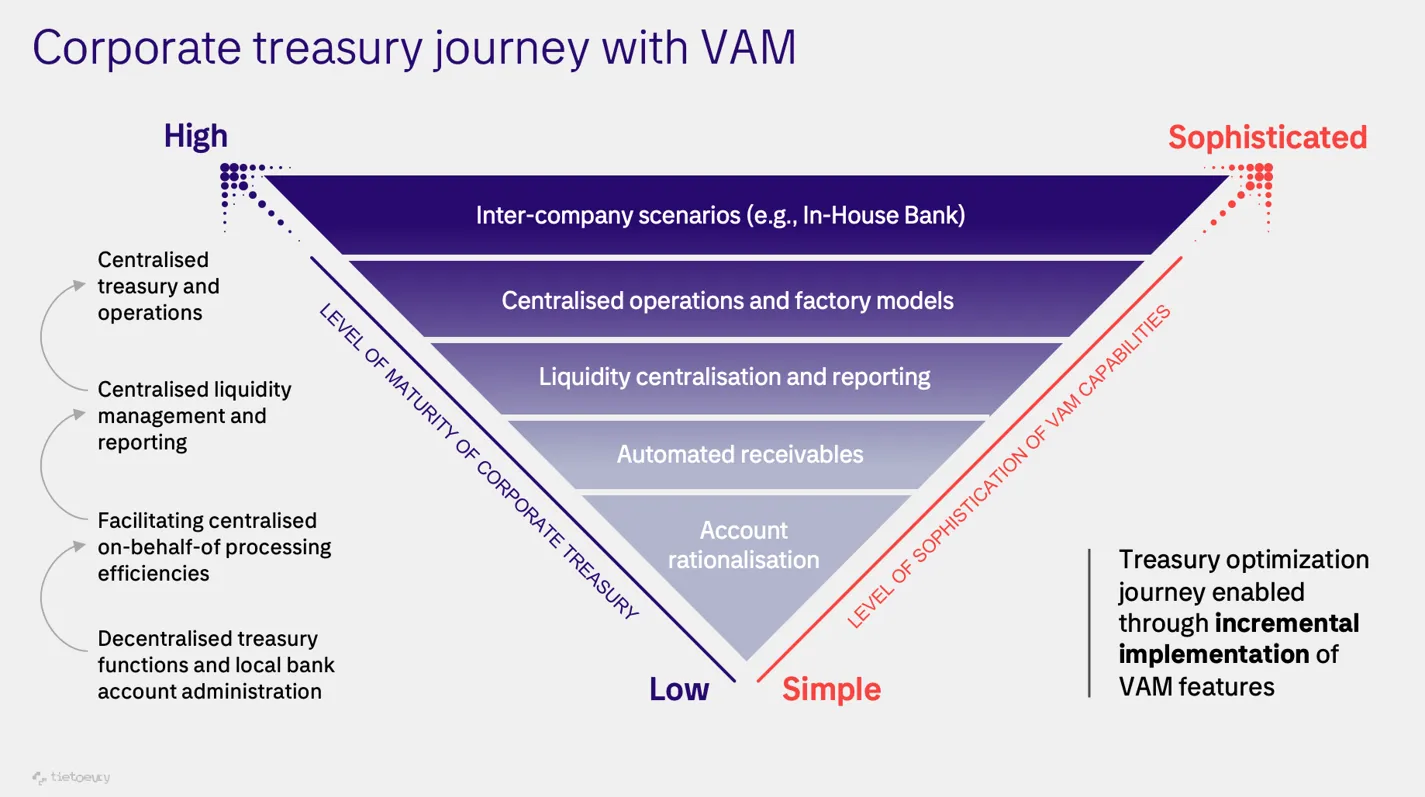

How virtual account management supports treasury transformation

Using tools such as Virtual Account Management (VAM), banks can provide the digital capabilities needed to support the transition from decentralized to centralized treasury structures.

Virtual accounts simplify, streamline, and consolidate treasury flows while improving cash visibility. Beyond account rationalization, they also support payments on behalf of (POBO) and receivables on behalf of (ROBO) structures.

When a treasury center makes or receives payments on behalf of a subsidiary, the transaction references the subsidiary's virtual account number. The transaction is reflected in both the virtual account and the associated physical account.

The corporate VAM journey is often implemented in phases, beginning with the organization's most pressing treasury needs and evolving toward more advanced intercompany scenarios, including a fully integrated in-house bank, as illustrated in Figure 2.

Figure 2

The role of banks in treasury digitalization

Not every corporate will choose full treasury centralization. However, understanding the available options allows treasury teams to identify where digitalization can deliver the greatest strategic value.

Some banks are now offering in-house banking as a service, recognizing that building an IHB from scratch can be costly, complex, and time-consuming.

By partnering with their banks, corporates can leverage existing banking capabilities and increase the likelihood of a successful, cost-effective transformation.

One of the biggest challenges during treasury transformation is integrating internal technology. Treasury data is often spread across multiple systems. Banks can help overcome these challenges through experience gained from similar client projects and partnerships with fintech providers that offer application programming interfaces (APIs) to simplify integration.

By combining technology, expertise, and banking services, banks can become valuable long-term partners in corporate treasury transformation.