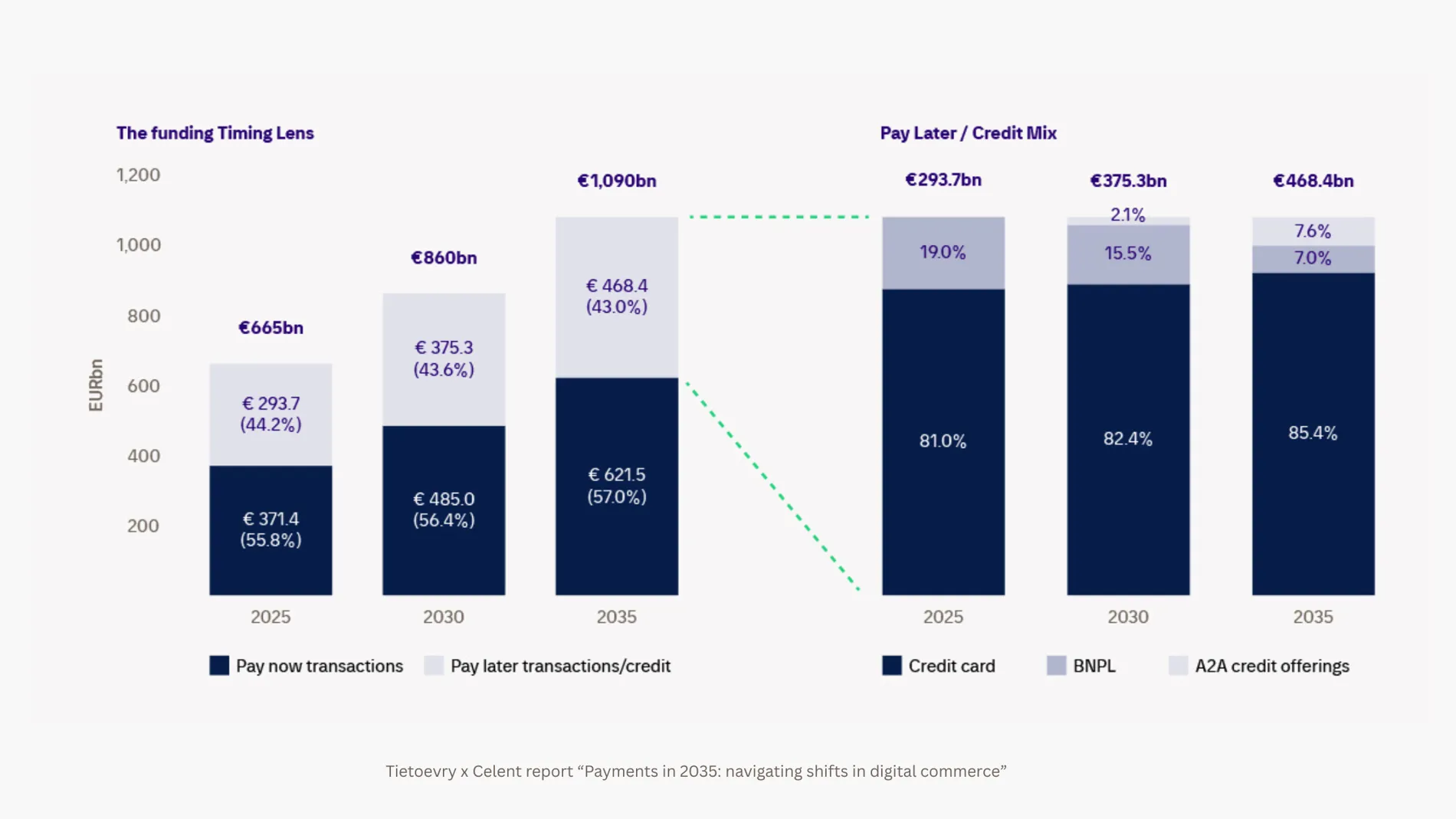

Rapid growth in digital payments driven by new payment types and credit options

The final driver is consumer familiarity and convenience. As consumers grow more comfortable with online payment and it becomes faster and more convenient, they will shop more online. According to the European Central Bank, online shopping as a share of all consumer spending volume hit 21% last year. By value, online transactions made up more than a third (36%) of all consumer spending, up from 28% in 2022.

How banks could respond

There are some clear conclusions for banks from the report “A Future of European Payments”. Most obviously, the trend towards higher online transaction volumes is only set to increase, especially if a-commerce agents begin to be used by consumers to shop on their behalf, a scenario which seems increasingly likely over the next decade.

Banks will want to ensure their payments platforms are able to cope with at least double the volumes they are seeing today, and that they can continue to deliver an outstanding user experience while managing higher volumes.

The ability to maintain service uptime 24/7/365 will also be key, alongside handling a wide range of transaction types – not just payment methods and rails, but high volumes of low value transactions as consumers go online for everything from subscriptions to low-value everyday items.

Faced with a wide variety of transaction types, banks will seek to maintain complete transaction and data security, a trend which implies a greater focus on financial crime prevention across all aspects of payments.

Finally, banks can expect the future to be more volatile and unpredictable, with transaction volumes that cycle through greater peaks and troughs. This makes the use of modern, cloud-native platforms that are ready to scale more important than ever.

For more on the future of European payments, download the report.